The ongoing U.S.-China trade war is likely to bring down inflation in the U.S. economy, key sections of the financial market indicate, offering bullish cues to risk assets, including bitcoin (BTC).

In his inaugural address on Jan. 20, President Donald Trump promised to “tariff and tax foreign countries to enrich our citizens,” and then fired the first shot against China, Canada and Mexico on Feb. 1. Since then, the trade tensions have escalated to such an extent that as of writing, the U.S. and China have imposed retaliatory tariffs on each other in excess of 100%.

Tariffs increase the cost of imported goods, which are then passed on to the consumer and could lead to higher general price level in a consumption-driven economy like the U.S.

Consequently since the trade war broke out, markets have been worried about a tariffs-led resurgence in the U.S. inflation, with the Fed adding to those concerns through its stagflationary economic projections last month. Stagflation, representing a combination of low growth, high inflation and joblessness, is seen as the worst outcome for riskier assets.

Bitcoin, therefore, has dropped nearly 20% since early February, alongside broad-based risk aversion on Wall Street that has seen investors concurrently dump stocks, bonds and the U.S. dollar.

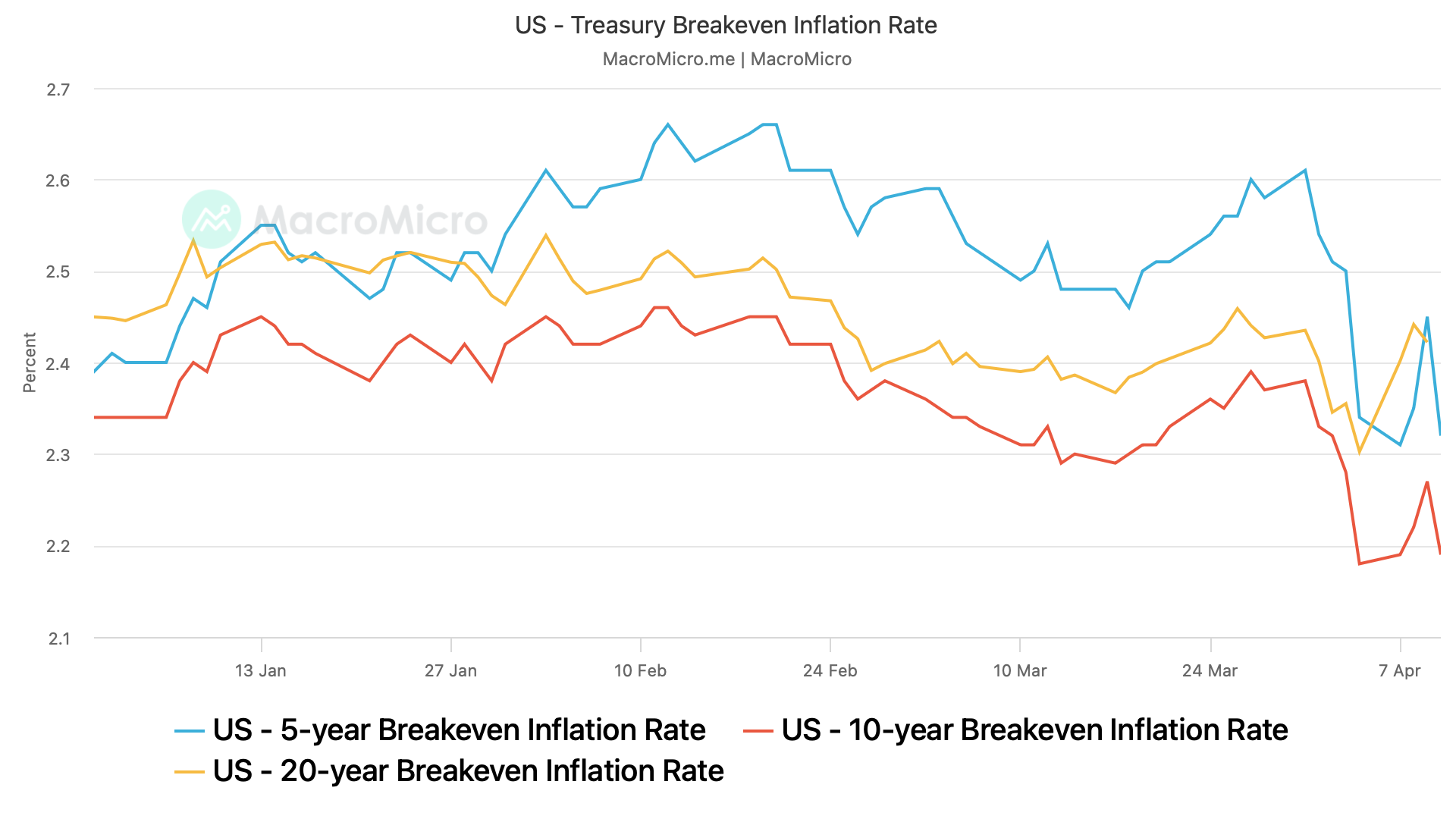

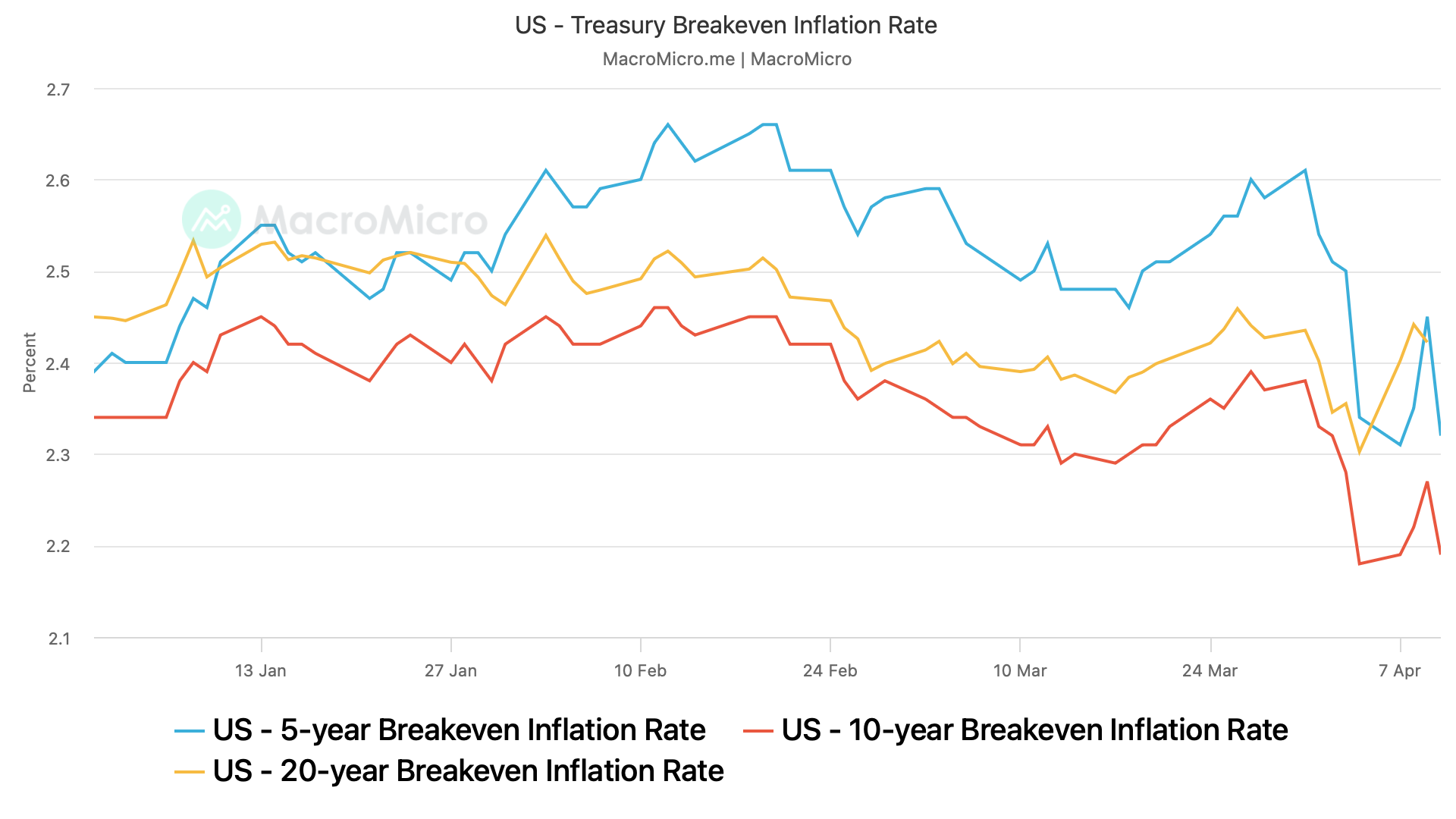

Breakevens suggest disinflation

However, market-based measures of inflation, such as the breakevens, suggest tariffs could be disinflationary over the long run. In other words, the Fed might be wrong in fearing stagflation and will soon have a leeway to cut rates.

Inflation breakevens the yields on traditional Treasury bonds with the yields on Treasury Inflation-Protected Securities (TIPS). The five-year breakeven inflation rate peaked above 2.6% in early February and has since dropped to 2.32%, according to data tracked by the Federal Reserve Bank of St. Louis.

The 10-year breakeven rate has dropped from 2.5% to 2.19%. Meanwhile, the Federal Reserve Bank of Cleveland’s expected two-year inflation has held at around 2.6%.

One time cost

According to observers, the impact of tariffs, viewed as a one-time cost adjustment, relies on the reactions of other macroeconomic variables and tends to be disinflationary in the long run.

When producers pass the tariff increase onto consumers, inflation levels rise. However, if there is no corresponding increase in income, consumers are compelled to reduce their consumption. This reduction can lead to inventory build-up and ultimately contribute to a decline in the prices of goods and services.

“Since the days of Smoot-Hawley, Tariffs have never been inflationary. Rather they are Deflationary and “stimulative themselves”. Moreover, the disinflation shown in these charts will help encourage the Fed to soon ease as well. The Calvary is coming!,” Jim Paulsen, author of the Paulsen Perspectives newsletter and a Wall Street veteran with four decades of experience, said on X.

A paper published by American economist Ravi Batra in 2001 made a similar observation, saying, “Tariffs in the US were never associated with rising prices, and trade liberalization with declining prices. High tariffs were always followed by sharp drops in the cost of living. tariffs produce inflation only in nonmarket or ualistic developing economies, but not inadvanced economies.”

All things considered, the recent financial market turbulence likely resulted from growth fears rather than inflation. The bull could soon reemerge in anticipation of a dovish stance from the Federal Reserve.

#BTC #Bull #Run #Ahead #Key #Markets #Trump #Tariffs #Bring #Inflation #Challenging #Feds #Stagflation #Fears

{kind=link}